This article discusses the methodology used for the construction and implementation of a balanced scorecard (BSC). The article is intended for business analysts, BSC implementation specialists and IT professionals.

Evaluating the need to develop a company strategy

In order to succeed in today’s dynamic business environment, companies need to quickly adapt to changing market conditions and outperform their competitors in terms of quality, service, the range of products offered and their price.

Only when management receives quick feedback on the company’s activities will it be able to make prompt and effective decisions. Operational activities must be coordinated and designed to achieve certain long-term objectives, otherwise companies risk falling behind their competitors. In order to achieve this, a company must be able to correctly identify its strategy and mobilize all available resources to achieve its strategic objectives.

Much in the way of company development depends on correctly and clearly formulated strategy. But it is also important to understand that a well-designed strategy is only half the battle, for it still needs to be successfully implemented.

So what does a company strategy look like? In all probability, no two companies see strategy in precisely the same way. Presentations on the topic may range from one slide with five keywords to an imposing document full of various spreadsheets entitled Long-Term Planning.

Many believe that content is the key to understanding of strategy and that the form in which it is presented is secondary. Yet managers are dropping this point of view since it is also true that company strategy can be successfully implemented only when it is understood by all employees. By presenting the corporate strategy in a more or less ordered, logical way, we increase the likelihood of its successful implementation.

One of the tools used to make the process of strategy implementation understandable is the Balanced Scorecard (BSC).

A balanced scorecard is a system of strategic management that measures and evaluates the effectiveness of a company based on a set of optimally selected measures that reflect all aspects of the organization’s activities, both financial and non-financial. The term "balanced" refers to the relationship that exists between short-term and long-term objectives, financial and non-financial measures, main and auxiliary characteristics, as well as external and internal aspects of company activities.

In practice, there are few examples of the successful implementation of a balanced scorecard, since when trying to implement it, one is faced with certain difficulties. One of the most common difficulties encountered when developing a BSC is the misunderstanding or misinterpretation of the methodology or organizational procedure. The sheer effort of developing a balanced scorecard and the absence of inexpensive and effective software applications are also impediments to its practical implementation.

The effectiveness of any balanced scorecard depends on the quality of its implementation. Balanced scorecard is implemented in four steps:

- Prepare for the development of a BSC;

- Develop a BSC;

- Cascade the BSC;

- Monitor strategy implementation.

Nowadays, strategy implementation procedures are almost always achieved via automation. The implementation of a Balanced Scorecard using, for example, Microsoft Excel, or in the absence of any information technology support whatsoever, is only possible at initial stages or in small organizations. Companies wishing to create and implement balanced scorecards for several departments in parallel and expecting to be able to periodically update and amend them will be unable to do so without the advantages of information technologies.

Currently, BSC developers have the following applications at their disposal: ARIS, Microsoft Office Business Scorecard Manager, and Business Studio.

Let us consider the methodology for implementing balanced scorecards in more detail. We will use Business Studio to illustrate the main stages of Balanced Scorecard implementation.

Prepare for the development of a balanced scorecard

At this stage, it is necessary to develop a company strategy and determine which organizational units and levels will be included in the balanced scorecard.

It is important to keep in mind that the BSC is a concept for implementing existing strategies, not developing fundamentally new ones. Once the strategy has been developed, it is possible to develop a balanced scorecard.

When deciding which departments to feature in the Balanced Scorecard, it should be considered that the greater the number of company departments that can be strategically managed via a single BSC, the greater the opportunity to cascade (decompose, transfer) important objectives from upper to lower levels.

One of the important activities to take place at the BSC preparation stage is the selection of perspectives.

Strategy development models can only be complete if they contain answers to issues relating to different areas of a company’s activities.

Simply setting financial objectives when implementing a balanced scorecard will not be sufficient if it is unclear how such objectives are to be achieved. Similarly, the objectives should not be completely isolated because in this case there is no information about how they influence each other. This implies the need for all important aspects of the company to be taken into account.

A scorecard is considered to be balanced only in case various perspectives are taken into account. To get a comprehensive overview of the company’s activities, strategic objectives, measures and initiatives should be developed based on a range of perspectives (Fig. 1).

Figure 1. BSC perspectives

Note that one-sided strategies are not necessarily focused exclusively on financial considerations. Some companies are overly customer-focused and forget about their financial objectives. Some companies may be overly focused on their business processes and pay little attention to market activities. The introduction of a balanced scorecard helps to avoid such bias by ensuring that equal consideration is given to the full range of perspectives.

Based on their empirical research, Robert Kaplan and David Norton have shown that successful companies take at least four perspectives into account when developing their BSCs:

- Financial perspective;

- Customer perspective;

- Internal Process perspective;

- Learning and Growth perspective.

These four perspectives are intended to provide answers to a set of questions, namely:

- The Financial perspective: How should we present ourselves to shareholders in order to achieve financial success?

- The Customer perspective: How should we present ourselves to customers in order to realize our vision of the future?

- The Internal Process perspective: In which business processes must we achieve excellence in order to meet the needs of our shareholders and customers?

- The Learning and Growth perspective: How should we maintain our ability to change and improve in order to realize our vision of the future?

It is the simplicity of these BSC perspectives and the presence of clear, logical relationships between them that makes it possible to deliver understanding of the processes taking place in a company to actors.

Develop a balanced scorecard

First, a Balanced Scorecard should be developed for only one organizational unit. This can be the whole company in its entirety, a subdivision or a department.

Irrespective of the size of the unit, the BSC is developed by performing the following steps:

- Specify the unit’s strategic objectives;

- Link the unit’s strategic objectives with cause-and-effect chains, i.e. design a strategy map;

- Select measures and determine their target values;

- Develop a set of strategic actions.

Refining bsc strategic objectives

Figure 2. BSC strategic objectives

Generally speaking, objectives are understood to be descriptions of the desired state of something in the future. Objectives can therefore be expressed in words, e. g., “Deliver our products to the customer within the shortest possible time". Measures and their target values can make the wording more precise, such as “within less than 36 hours".

Strategic management system implies decomposition (breaking down, structuring) of a company’s general strategy into specific strategic objectives that reflect various aspects of the company strategy in detail. Integration of individual objectives establishes the causal relationships between them so that the full set of objectives completely reflects the company’s strategy.

Each of the company’s strategic objectives is associated with one of the development perspectives of the organization.

Defining too many strategic objectives for the top level of the organization should be avoided. A maximum of 25 objectives is normally sufficient. Too many objectives in a scorecard indicates that the organization is unable to focus on the essentials; it also means that the stated objectives will not be strategic at the organizational level for which the scorecard is being developed. Tactical and operational objectives are served by the measures of corporate departments located at lower levels in the organizational structure.

Designing a strategy map

Determining and documenting the causal relationships between individual strategic objectives is one of the core concepts of BSC.

The cause-and-effect relationships established reflect interdependencies of individual objectives. Thus it is clear that strategic objectives are not in fact independent of each other; on the contrary, they are closely related and influence each other. The achievement of one objective makes a step towards the achievement of another one, and so on, right up to the main objective of the organization. The cause-and-effect chains (Fig. 3) are a clearly visible demonstration of the relationships existing between various objectives. Those chains that do not contribute to the achievement of the main objective are excluded from further consideration.

The cause-and-effect chains are a handy tool for taking BSC down to the lower organizational levels.

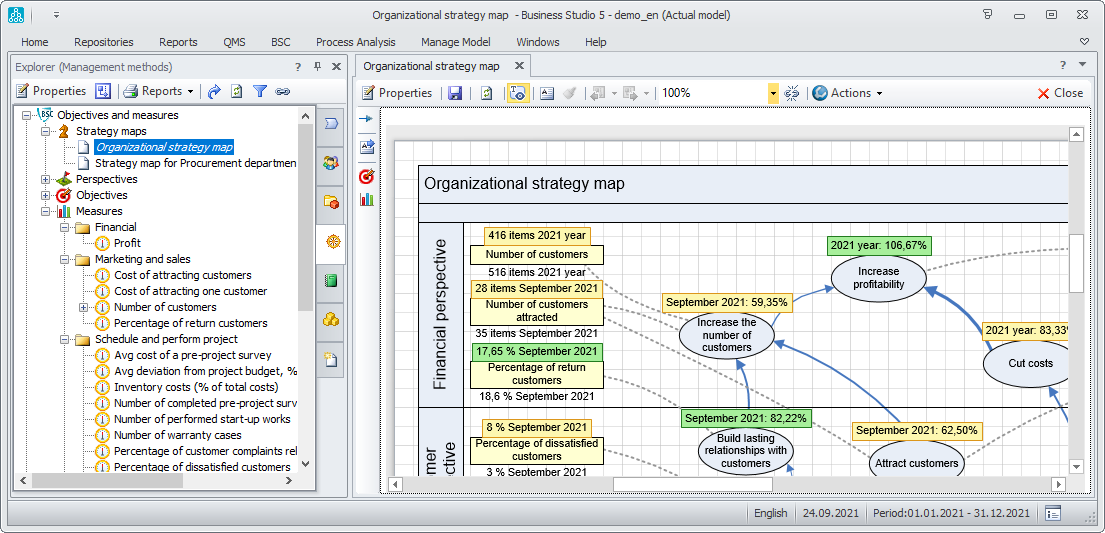

The strategy map is used to graphically display relationships between the company’s strategic objectives and the BSC perspectives.

Figure 3. Cause-and-effect chains linking strategic objectives

How to measure achievement of strategic objectives

The BSC measures (shown as rectangles in Fig. 3) are objective measurement devices. Measures are used to evaluate the degree of progress made towards the achievement of a particular strategic objective (Fig. 4).

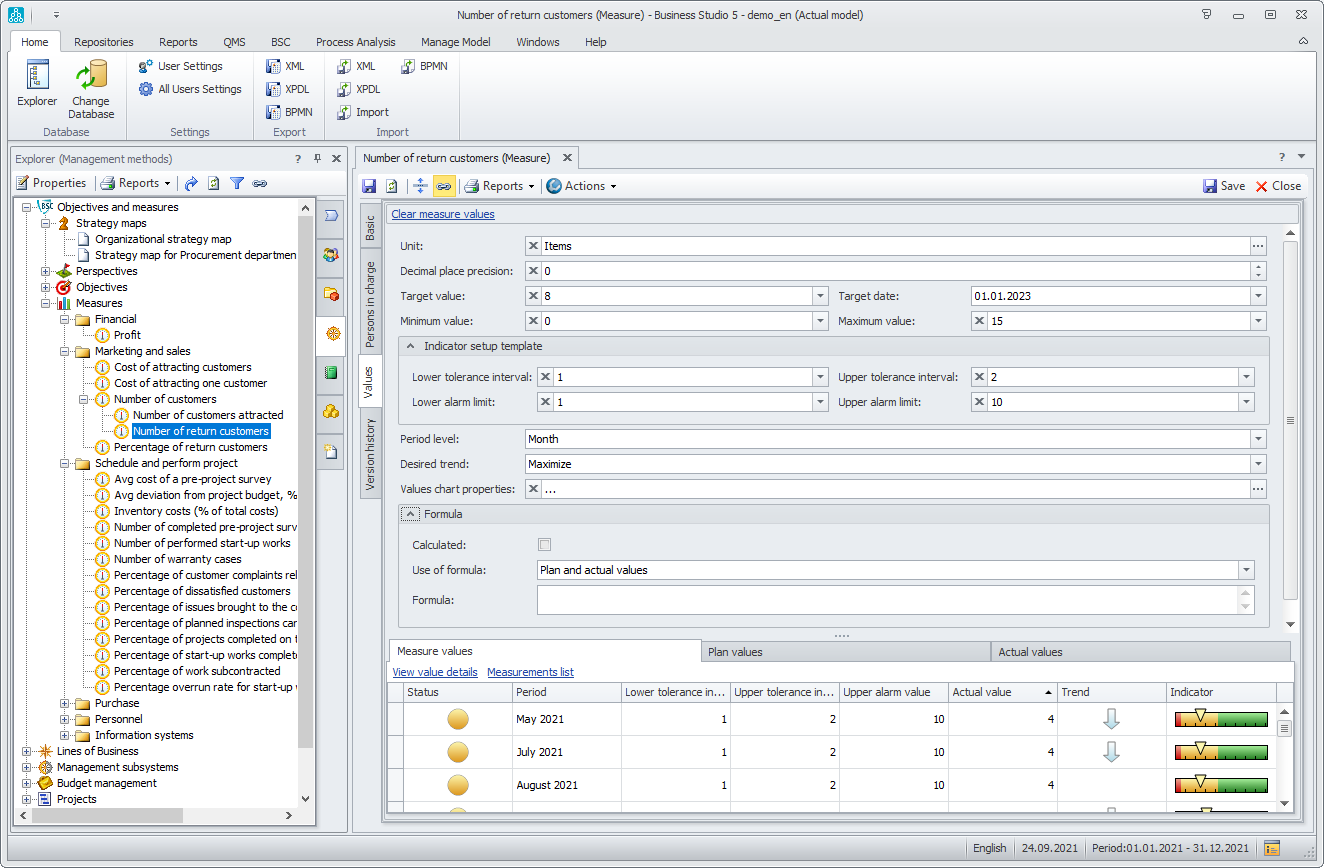

Measures are a way of substantiating the system of objectives developed at the strategic planning stage and making those objectives measurable. Measures can only be selected once the objectives are defined. But selecting the precise measures is a secondary issue, since even the best measures cannot help a company succeed if the objectives have been defined incorrectly. No more than two or three measures should be used for the measurement of each of the strategic objectives.

Without target values, the measures used to evaluate strategic objective achievement would be meaningless. Determining the target values of objective achievement measures can be tricky, and not only in procedures relating to BSC development. The main difficulty is to set an achievable target value.

As a rule, a balanced scorecard is developed for a long-term strategic period (3–5 years). And target values are set for the lagging measures that measure achievement of ultimate objectives of corporate strategy. But since the company strategy also needs to be measured over shorter periods of time (1 year would be considered a medium term), target values are also set for leading measures that measure achievement of shorter-term objectives. This results in a balanced scorecard measuring both long-term and short-term objectives.

In Business Studio, depending on the particular objective, short-term planning is based on the quarter, month, week or day and is expressed in terms of plan measure values. Measures and their associated target values are used to warn management of any deviation in the operation of the company from its planned strategy at the earliest opportunity, i. e. the actual results achieved by the company are compared with the target values.

As previously mentioned, a measure is a way of evaluating the degree of objective achievement. However, it is also a tool that can be used to assess effectiveness and efficiency of a given business process. Thus measures are used to assess effectiveness of business processes and achievement of objectives simultaneously.

Figure 4. BSC measures

Strategic actions taken to achieve strategic objectives

To achieve strategic objectives strategic actions are to be taken. "Strategic actions" is a general term for all activities, projects, programs and initiatives undertaken to achieve strategic objectives.

Relating company projects to strategic objectives allows to reveal the extent to which any particular project or initiative contributes to strategic objective achievement. Initiatives that do not contribute to strategic objective achievement may nevertheless be contributing to the achievement of objectives elsewhere in the system. Where this or that strategic initiative makes no significant contribution even to the achievement of a lesser objective, then it is doubtful that the initiative is worth implementing.

Cascade the balanced scorecard

Cascading is a method used to improve the quality of strategic management in organizational units involved in developing Balanced Scorecards. Objectives and strategic initiatives of highly-placed org units are consistently transferred to the BSCs of units positioned lower down the system; this is known as the vertical integration of objectives.

When cascading, the strategy outlined in the company’s Balanced Scorecard is applied to all levels of management. The relevant strategic objectives, measures, target values, and improvement initiatives are then determined and adapted to suit all departments and teams. In other words, the company’s Balanced Scorecard must be linked to the BSCs of departments and subunits, as well as to the working procedures of individual employees. Each and every department develops its own BSC based on that of the division to which it belongs and coordinated with that of the company as a whole. Each and every employee then develops their own individual work plan together with their Department Head. This focuses minds on achieving real results in the workplace rather than on tasks and initiatives aimed at improvement.

Thus cascading is a way of building bridges between the various levels of corporate hierarchy, which can be used to transfer corporate strategy from the top level to the bottom.

Monitor strategy implementation

In order to update and improve it, the balanced scorecard should be continuously reviewed and evaluated by upper management and those responsible for company performance.

Strategic objectives are of the greatest relevance to the performance of the organization and should be assessed at least once per year. When doing so, the following questions should be answered:

- Are the selected measures suitable for assessing the defined objectives?

- How easy is it to calculate measure values?

- Has the given department already achieved the target values of measures?

- Have the target measure values of more highly-placed departments already been achieved?

- How does the given department contribute to the upper-level objective achievement?

Measures are assessed primarily to discover whether the actual value can be calculated on the basis of the data for the reporting period. It also allows the plan and actual values to be compared and the causes for their deviation to be determined. These analyses are accompanied either by the adjustment of the target measure value or by the development of corrective actions aimed at achieving the previously established target value.

The BSCs of lower-placed organizational units should always be checked to establish whether or not they are contributing to the high-level objective achievement.

It is always advisable to forecast target values for the longest possible periods of time.

What are the benefits of implementing a balanced scorecard?

Let’s summarize our findings thus far. What are the company’s benefits of describing and implementing its strategy using the Balanced Scorecard methodology? First and foremost — and most importantly — the knowledge that the company’s efforts are being focused in areas of strategic importance. The goal of the company is determined, the means of achieving it (the strategic objectives) are defined and cascaded through all departments. Second, each and every department has its strategic objectives, so everyone in the company understands what needs to be done. Third, the system gives management a clear understanding of the effectiveness of the company activity. Objective achievement measures allow all process participants to understand their role in the implementation of the company strategy. The fourth and final result is top to bottom control of the strategy implementation process. In short, a company becomes an effective instrument for achieving the goal established by shareholders.

Advantages of computer technologies

All of the above is completely achievable without any automation. Moreover, a number of successful businesses were using similar techniques in the late 19th century, when computer technologies were unavailable. But can powerful computing technology and automation somehow make strategy implementation more effective? Of course, not using such technology doesn’t imply resorting to a pencil and paper. The collection of data and some measure processing procedures can be carried out simply using Microsoft Excel. However, it must be remembered that the company’s strategic objectives may change, the significance of some measures will turn out to have been overestimated, elements we considered to be unimportant will start to become decisive... A manager should be able to reach to the changes and correct their plan as quickly as possible, for each and every time we step out in the wrong direction, we are distracted from our ultimate objective.

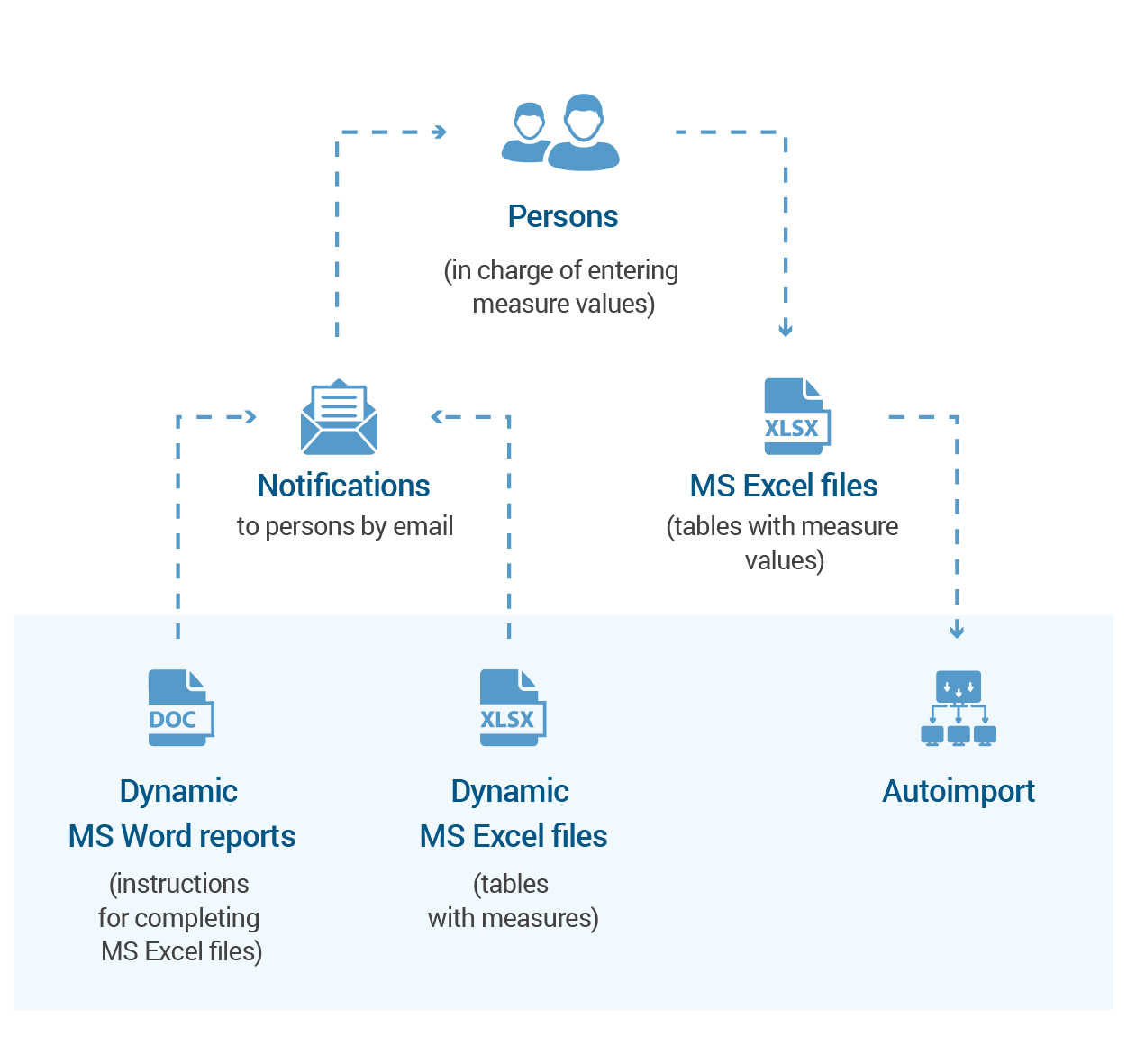

The main problem faced by companies when implementing this methodology is not how to automate the creation of objective and measure tree or design a strategy map but how to automate the constant stream of new data required by the BSC. Without this, operational control over the implementation of the strategy is impossible. For example, measure values can be collected using the mailing system in Business Studio (Fig. 5). The values of measures not entered in the information system are collected using Microsoft Excel files, which are automatically sent out to responsible employees and subsequently imported into the system.

Those responsible for entering measure values into the system are sent a dynamic letter with instructions on how to present the data. Business Studio automatically finds and lists all the measures belonging to any given employee and generates a Microsoft Excel file for each, together with tables for entry of the data. This file is attached to the letter and sent out automatically to the email address stored for the employee in the system directory.

Figure 5. Collecting measure values by email

Responsible employees complete the tables with the actual measure values and then either save the file to a specified folder on the server or send it to the system administrator. The system automatically reads the files in the specified folder and loads the data into a dedicated database. This marks the end of the measure value collection stage.

The balanced scorecard must, like any other management tool, be adjusted to suit changes both in the company’s development and the external environment. The environment in which companies operate is normally very dynamic and this results in the need to change the organization’s strategic objectives. This, in turn, means continuous update of the relevant objective achievement measures. Failure to update the measures not only makes the BSC system unworkable but can also damage the company’s operations in the worst-case scenario.

The collected measure values are normally provided for shareholder analysis. To facilitate this, the system has a set of pre-configured report templates which, if necessary, can be either changed or supplemented by new ones. The changes of plan and actual values of various measures are presented in periodic BSC reports. Users are able to select the reporting period in the Business Studio system settings.

* * *

Nowadays companies operate in a very competitive environment, and it is vitally important for any company to constantly improve efficiency of its activities. Management activity is no exception. Managers need the tools to do their job just like any other employee. The techniques described above may seem complicated, but their complexity is completely offset by their effectiveness; the availability of software tools for their implementation means the work can be performed in real time.

October 2021

Share